") The server business last year netted vendors $ 34.4 billion on sales of 8 billion servers according to IDC, but those numbers don’t show how that business is changing. For that compare the growth in the traditional x86 market that sold those 8 million servers which grew a mere 3.7 percent year over year, to what IDC calls the densely optimized servers used in webscale deployments. That segment grew by 51.5 in units sold, and now represent 3.2 percent of all server revenue and 6.1 percent of all server shipments.

The server business last year netted vendors $ 34.4 billion on sales of 8 billion servers according to IDC, but those numbers don’t show how that business is changing. For that compare the growth in the traditional x86 market that sold those 8 million servers which grew a mere 3.7 percent year over year, to what IDC calls the densely optimized servers used in webscale deployments. That segment grew by 51.5 in units sold, and now represent 3.2 percent of all server revenue and 6.1 percent of all server shipments.

While plenty of companies spend money buying gear from IBM, HP and Dell, others are going direct to the companies that build servers for those giants. For companies such as Facebook, Baidu, Zynga, Amazon and Facebook are building at such scale, the idea of wasting a single cent or milliwatt on an unnecessary feature or frill is economically and ecologically stupid.

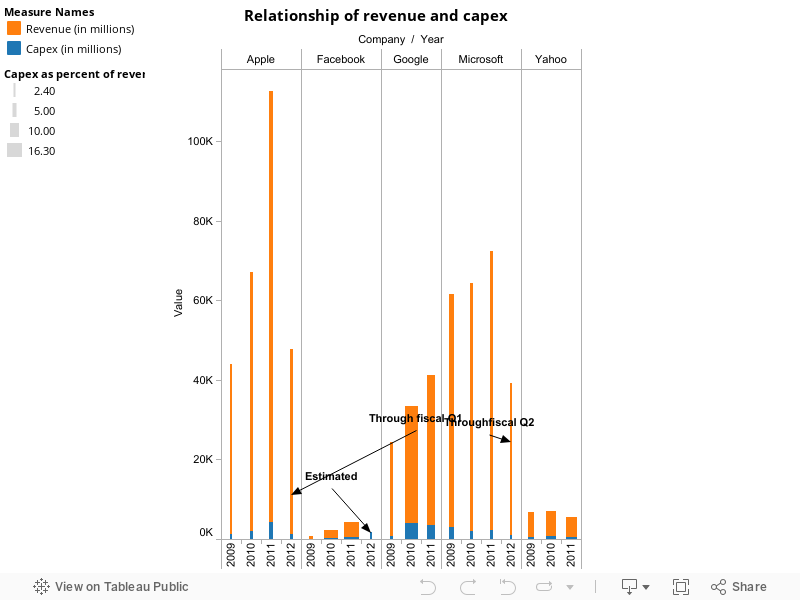

Many of these web scale companies have businesses that depend on the IT to deliver their product — a webpage or ad — that generates a few cents each time a user loads the page. Cutting costs in IT has huge effects on the bottom line. For example, Facebook spent 16 percent and Google both spent about 9 percent of its revenue on infrastructure and capital expenditures in 2011.For details read the GigaOM Pro item on the topic, found here (subscription req’d).

More infrastructure, more users, less money.

What’s occurring here is a shift in the value of a server, and thus of server makers. What used to be high-end machines with features driven by the engineers inside Dell, IBM, HP, etc., have now become a commodity, and not a Dell-like commodity either — a really low-end commodity. These servers are stripped-down machines custom-built by the guys who built Dell’s and HP’s boxes. The rise of Quanta has begun.

This rise was a direct result of the industry refusing to listen to the demands of its customers, especially because those demands didn’t seem to involve a way for the server guys to make much money. At first, Rackable, now called SGI, picked up on the business, but as Forrest Norrad, the VP of servers at Dell pointed out on Wednesday at the Open Compute Summit, Dell realized that companies like Facebook were not just one-off complainers. They were the leading edge of a new way of doing business– and IT was a fundamental element of that business.

So Dell created its DCS group in 2006 to serve customers buying more than 2,000 servers at time. When that group began, Dell estimated that the webscale server market was perhaps 4 percent of the market. Today, Norrad says its about 20 percent of the market. And it’s growing. So while traditional enterprise servers might be that $ 34.4 billion a year business, that business isn’t where the growth is. Check out this illustration shown by Facebook’s Frank Frankovsky for where he thinks the real growth is.

Throw the server vendors a bone and let’s keep moving.

And here’s where the Open Compute Project comes in. Unlike DCS, which was a successful effort to serve the market once Dell had validated it, the Open Compute Project is a coup by the buyers of servers to take control of their hardware destiny. As such, I wondered if this coup would leave room for Dell or HP to continue to build their businesses. After attending Wednesday’s Open Compute Summit, I can say it seems like it will.

From the talk of creating “innovation zones” within the Open Rack design where vendors can try to create value above and beyond the Open Compute standard, to the AMD and Intel motherboards that were created with the financial services industry, it seems like vendors can work within the confines of Open Compute and still see margins. We’ll have to see what those margins are, but neither HP nor Dell are betting solely on hardware. Both are making big plays into software and services associated with the webscale market as they adapt not just to the changes in servers, but also to the overall change in IT.

Is this a mainframe transitions or a miniPC transition?

Going forward, the question that should keep the industry up at night is how the infrastructure market will shake out and how quickly this will happen. Norrad says he’s wondering if the legacy enterprise servers will be more like mainframes or more like the mini PC. Mainframes are still around (and super profitable), although not at all a growing business, while mini PCs have all but disappeared. For the legacy gear vendors, the question is will the enterprise server business stick around, even if it doesn’t grow, or will it die out?

The next obvious question is how fast this transition will happen. If this is a rapid shift, companies like Cisco, HP or IBM risk having significant portions of their businesses erode seemingly overnight. If the transition is slow, then vendors can take their time buying promising startups, working with efforts like Open Compute and building up their services or other lines business. So far, the consensus on how fast a shift this will be is mixed, but everyone agrees that transitions happen faster now and that the rise of an open source hardware framework will accelerate it. This will be an ongoing topic of conversation at our upcoming Structure 2012 conference held this June in San Francisco.

Even Open Compute lets vendors like Dell and HP maintain a profit margin, the bigger story here is how servers are no longer the cornerstone of an IT strategy. As our data centers get bigger and the needs of webscale and cloud providers take over more of the industry, servers are mere components of a much larger machine. While components can be valuable, they are no longer the entire system and as such their value can’t be divorced from the data center where they sit.

This means companies must start with a commodity and really work to add value, not just cool features. Historically, the infrastructure business hasn’t been good at this. Maybe it’s learning.

Related research and analysis from GigaOM Pro:

Subscriber content. Sign up for a free trial.

- The capex connection: Why we pay for privacy on the Web

- Infrastructure Overview, Q2 2010

- Infrastructure Q3: OpenStack and flash step into the spotlight

![]()